How Sportsbook Apps Incinerate Cash

How Sportsbook Apps Incinerate Cash

Losing money even when the game is rigged.

To understand the sportsbook betting apps it’s useful - and fun - to explore the story of Las Vegas first.

Vegas became Sin City in the wake of the Second World War. The state of Nevada legalized casino gambling back in 1931 but given the whole depression and war thing, it took a while to take off. When it did, the city’s gambling activities were widely controlled and run by organized crime.

At first glance, it is not at all obvious as to why legal gambling in Vegas ought to have been run by the mob. The whole point of being the mob is to engage in illegal activities that garner outsized economic returns due to their associated risks. However, gambling is a strange affair due to one key factor: contracts.

In general, gambling is merely the contracting between two or more parties regarding the possible outcome of an event. One party says X, the other says not-X and there are agreed-upon odds which one of the parties will be liable for. You would think that given the contractual nature of gambling that any outstanding debts would be dealt with within the court system. However, you would be wrong because gambling doesn’t work like normal contracts.

There are two types of gamblers who make or break a casino’s financial performance. The first are – for lack of a better term – degenerate gamblers. This category of clientele is more or less addicted to the endorphin chase that arises from hitting it big. All of their cash, whether from a job or their Social Security checks, goes into the slot machines or onto the roulette table. These folks are the passive income backbone of gambling establishments.

If you’re walking through the Venetian and you see a visor-wearing grandma with a fanny pack of cigarettes smashing away on a Katy Perry-themed penny slot then you have seen this archetype in the wild.

Then there are the whales. These are folks who frankly have more money than they know what to do with. For them, gambling is not about winning – it is about consuming. They come into town, stake $ 20 million into their account at Mandalay Bay, and then let the hotels take care of their every whim at no additional charge.

Every driver in Vegas has a portfolio of stories about these gamblers. The stories are almost always fiction but the fact of the matter is that they are plausible. In terms of specifics they are false but broadly speaking they convey a truth regarding what the casinos are willing to do.

Back in the wild-ass days of the George W Bush administration, I was all of 12 years old and on a family vacation to Vegas. [Sidenote: we all seem to have forgotten how fucking nuts we as a society went in the early 2000s. Back when we had Hummers, low-rise pants, and dreams.] Anyway, the cabby from the airport regaled my family with the story of a Saudi prince who came to town, put eight figures into his casino account, and then had the good folks at Caesar’s take his wife and children to Disneyland for the week while he rolled with the big dogs. Again, definitely a constructed fiction but a plausible one indicating the state of affairs nonetheless.

Back to the matter at hand here. These two types of gamblers are wildly different in how they are treated by their counterparties in the event of outstanding debt. With the whales, the casinos mitigate risk by having them deposit most – if not all – of their available gambling funds up front and then they assign staff to them to ensure that they do not blow up beyond the equity in their accounts. With the degenerates though, this is where things get dicey, and formal contract enforcement goes to shit.

Degenerate gamblers have to gamble. If not, they will act like any other addict when you suddenly remove their fixation. For the riskiest ones, this leads to them taking out loans if they are short on cash. No bank is going to lend them money for this. Hell, pawnbrokers and payday loan companies would even whiff on taking up such a risky client. So in comes the mob.

The mob does not – for obvious reasons – deal with the court system when it comes to most debts. Instead, they deal in broken bones and shattered knee caps. If a degenerate does not pay their debts then fixers will ransack their rooms, go to their house, and take any form of collateral they can. While the high-end clientele in Monte Carlo might not need the threat of violence to make good on their debts, the degenerate income stream requires some omelet-making, if you know what I mean.

Hence, the mob – if gussied up appropriately via fancy shindigs and grand casinos – was able to attract money from both the whales and the degenerates. That was their secret sauce in terms of founding the Vegas we know today.

The enforcement component of gambling goes back an awful long way and I would argue that it is inseparable from the act of gambling itself. Either we are all saints – in which case we wouldn’t be gambling in the first place – or we require contract enforcement mechanisms.

The basis for needing enforcement is that book runners (the folks who make odds and take bets) are in the business of market-making. This means that they will take bets that are not offset on the other side from time to time in order to facilitate betting. If a bookie gives ten-to-one odds that the Patriots will beat the Browns and someone takes that bet, the bookie is at risk of having to pay out from their own pockets in the event of a Patriots win. It’s their job to make sure that they find enough people taking the other side of the bet to transfer payout risk [also known as liquidity risk].

It is important to note that this risk can only be transferred if the person accepting the risk is able to pony up the cash for it when it comes time to pay the piper. Part of a bookie’s ‘service’ can be that you can call in a bet. In this situation, you hit up the bookie and they place a bet for you using their own cash. In the event that you win, they take their fee from the spoils. If you lose though, they are immediately on the hook for your debt, which means that you’ve entered into a classic ‘bitch better have my money’ scenario.

The person on the other side of the bet – who just won your money – needs to be paid immediately, meaning that your bookie can’t file a claim against you (assuming that such gambling is legal in your jurisdiction) in court. That would take months, if not longer, to get through the system. Plus there are legal costs that chip away at the bookie’s eventual payment. Instead, the bookie will use enforcers from the mob who will collect what you owe as soon as they find you. Thus, the bookmaking business is a natural habitat for organized crime. If you’ve ever seen the Netflix series Peaky Blinders, this is why the various gangs run the bookies at the pony tracks.

Now, to return to Vegas here. The mob was the natural owner-operator of the casinos so long as the focus was solely on gambling. Or rather, we can imagine that there is a fixed pie of revenue associated with gambling. The pie can grow but each component part (i.e. degenerate, whale, and other) grows in equal proportion. So long as the degenerate portion is chased after by the casinos for revenue, there is a strong need for enforcement amongst the riskier clients. As soon as alternative revenue streams become available at a lower risk rate then the casinos can cease to chase the riskiest degenerates.

Initially, more or less, everything was free in Vegas at the casinos. Your room, food, drinks, and entertainment were complimentary so long as you gambled. The more you gambled the nicer the shit they gave you. Big rollers were put up in the penthouse while the degenerates had creaky twin-sized beds. Once non-mob business folks began to realize how lucrative the casino business was in Vegas, they turned their sights on getting a slice of the action.

‘Legitimate’ business folks were not too interested in busting balls and cracking skulls. So o they looked for new revenue opportunities in the form of charging for rooms and food. Sure, so long as you’re sitting at a slot machine – and tipping well – they will comp you free drinks, but otherwise, you’re on the hook for your room and board. This allowed the casinos to drop their riskiest players and associated lending and enforcement.

Eventually, Howard Hughes came in and started to buy out the mob and Vegas itself changed with its new owners. The degenerates stayed but they could no longer use the house as a kind of piggybank of last resort. Loan sharks still exist but they are found down dark alleys beyond the light of legitimate businessmen or in the hell hole known as ‘fintech’. These changes were all about becoming increasingly legitimate businesses while reducing the risk profiles. Out went the broken knees and in came Elvis.

While the whales are certainly an interesting group of folks to think about, I’m more interested in the degenerate gamblers. Why? Because most of us, if provided the circumstances and opportunity would find ourselves in the degenerate camp versus the whale cohort. Additionally, the degenerate folks are indicative of the crowd that engages in daily fantasy and the emerging sportsbook crowd of companies.

The apps peddled by likes of DraftKings, FanDuel, Barstool, et al., are designed for the degenerate gambler. If I’m an Italian whale looking for a reason to go to confession next week, I’m not going to do it from my phone. I’m going to get on my private jet and go roll some dice in the desert. Meanwhile, the average Joe can skimp on the airfare and risk it for the biscuit from his couch.

Let me just get it out of the way here that I do not take a moralistic approach to gambling. It is what it is. I don’t gamble but that’s because I get my endorphins elsewhere. What I’m interested in is exploring what it means for these new gambling platforms to be degenerate-focused and whether or not they actually make sense as a business proposition.

The premise of these new sportsbook platforms is that they allow normal folks to bet on the outcomes of sporting events from the comfort of their homes with the convenience of their phones. Once a gambler gets acclimatized to a given platform, they will – in theory – use that platform for all of their needs.

The basic business proposition – I shit you not – is that everyone has some level of constant or regular desire to gamble. Let’s say that John Doe has a risk appetite equal to 3% of his salary. All he needs is a fun and convenient way to spend that 3%. If you make a shiny app that’s hip and cool [as the youths say] then he is highly likely to spend that 3% on the platform. From the perspective of these new sportsbook apps, John – who let’s say makes $100,000 a year – is worth up to $3,000 per annum to them.

Every sportsbook app has a model of lifetime customer value. There is a generic customer value for non-activated users who have yet to download the app. This value is about $0. With each additional step taken the customer value rises. If someone downloads the app, suddenly they are worth a lot more. If they deposit cash into their app account then they are worth a pretty penny. If they place their first bet, the value goes up. If they win a bet, the value will pump onwards and upwards. Therefore, it is in the interest of these firms to get folks to do four things: download the app, deposit cash, place a bet, and place more bets until they win one.

How do you get someone to download the app? You advertise like hell across likely channels of interest. This is why FanDuel was the presenting sponsor of the Bill Simmons Podcast and why you can’t turn on the US Open without being slapped in the face 47 times by sportsbook commercials. Not to mention the promotion of gambling content from banner ads to segments during Sportscenter. All these efforts aim to get folks to download the damn apps.

Once you download the app you get hit with offers of ‘risk free bets.’ These offers are almost always contingent on users depositing a certain amount of money into their accounts. This is a genius move. It checks the second and third value-adding items off the list. If money is put into the account then in all likelihood, the user is going to gamble that amount after the risk-free funds are used up. The risk-free offer means that the user will learn the ropes of placing a bet with ‘no’ downside. Hell, they might even win.

If the barrier to use is broken down by the risk free bets then the user is increasingly likely to try to win. The odds are always against you in gambling so the user is going to lose a couple times at least before they win. By losing, the user gets a desire for revenge or vindication. If they do not walk away after a few, then they will wager in search of a win up to their risk tolerance. If they win, then they have received positive reinforcement for their actions. It’s entirely likely that at this point the user is moderately committed to sports betting as either a past time or something more.

The value of these platforms comes from customer acquisition. The largest movement in customer value comes from that initial step of downloading the app. The value moves from effectively $0 to something above that. Basic math tells you that this represents an infinite percentage increase in value.

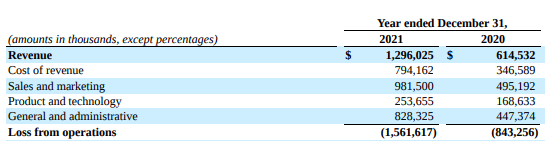

Additionally, each further value-increase is dependent on that first downloading of the app. It should therefore come as no surprise that these platforms trip over themselves in order to spend ungodly amounts on customer acquisition. For example, the image below shows the impact of DraftKings’ Cost of Revenue and Sales and Marketing efforts on their operational bottom line:

In short, DraftKings is spending more on acquiring new customers than it can make from its existing users.

From the same 10-K we see that in 2021 monthly paying users grew from 883,000 to 1,494,000. At the same time, the average monthly revenue per user grew from $51 to $67 dollars. These numbers look decent, right? Wrong.

If DraftKings has 1.494-million monthly users and they spent $981.5-million on sales and marketing, then they spent $656 per user. If we assume that the bulk of marketing efforts are for new user acquisition then in 2021 DraftKings spent something like $1600 per user acquired on marketing. Keep in mind that the average value per paying user is $67 per month or $804 per year. Therefore, the payback period for the marketing used to acquire these users is about 2 years. That’s of course if you ignore the costs of said revenue. Factoring that in at $531 per user leaves you with 2.65 years not to mention that general and administrative costs run you past 3 years. As you make your way down the income statement the payback period gets further and further away.

Someone might say that 3 years ain’t terrible, but for comparison, the automotive industry has a customer acquisition cost of $600-$700. Given that, for example, Ford has gross margins of around 6% on its auto sales in 2021 so long as it sells a vehicle for ten to twelve thousand dollars, the payback period is negligible using the back of the envelope method above. [Yes, I’m aware that this is the most back-of-the-envelope method possible but I’m here for the magnitude, not degree]

This is not to say that DraftKings is a notionally unsustainable business per se. If you compare their Cost of Revenue as a percentage of Revenue, with casino-only revenues and expenses of a traditional physical player like Wynn Resorts, you get similar proportions – 61% versus 65%. Not bad, but the marketing costs absolutely sewer the business. This raises the question of why the hell are they marketing so hard if they have a potentially sustainable business as is at over a billion dollars in revenues?

The answer is that they have to keep up the efforts in order to (1) keep growing the userbase, and (2) fend off competitors. If FanDuel drops a ton of capital on marketing then they will likely poach users from DraftKings. Same goes for every other sportsbook apps. Lost users means lost revenue which means they will certainly never make back the marketing expense associated with customer acquisition. The desperate situation is perhaps best encapsulated by the fact that they have to ensure that each user acquired in 2021 hangs around on the platform – at current activity levels – until 2025. Otherwise, the payback period goes to infinity for each user who leaves.

Normally I would say that this is a classic case of cheap capital subsidizing an existing business model in the name of ‘disruption’ but I don’t think that’s really what’s happening here. Instead, what I think has happened with these new sportsbook platforms is that they have shot themselves in the foot from the get go. Basically, their growth model precludes them from a functioning business model

The sportsbook apps’ strategies have focused on user growth. More users means more revenue. However, the competitive landscape has meant that users are hard to come by. As a result, the platforms are spending literal fuck tons of cash to acquire each additional user.

So long as user growth is the sole KPI this strategy is fine because it is a ‘grow at all costs’ mentality. Once the KPI shifts to something like earnings, profits, and cashflow, the companies find themselves in a hole they can’t get out of. At current levels, existing users simply do not spend enough on the platforms to justify their initial acquisition.

I cannot stress this enough – existing users on platforms like DraftKings are liabilities not assets. Yes, they have asset qualities like positive future cashflows, but they have to stick around long enough to pay off that initial acquisition cost. The need to keep them in the system means that you end up adding additional marketing costs to keep them from jumping over to a competitor.

The only way that a platform like DraftKings can turn the ship around is to acquire enough users at a much lower cost of acquisition. These users will pay themselves off more quickly and then will be able to contribute to paying off the sunk costs associated with the acquisition of older users. There is no reason to see this turnaround coming anytime soon given the ongoing competitive landscape. The more potentially profitable the sector becomes the greater the incentive for new entrants offering the same upfront bonuses.

This brings us back to the Vegas narrative. These platforms are not for whales. They are for degenerates or those who could reasonably become degenerates someday. As such, these platforms carry a higher risk profile than traditional casinos. This profile is not in any way reduced through diversification efforts like accommodations, food, and live shows. As of right now, these platforms do not operate like the Vegas shops of old. They do not typically lend users credit per se. At some point though, these platforms will get into the loan game. Or at least that’s my prediction. Why? Because the riskiest degenerates are possibly lucrative.

I guarantee you that some investment banker or consultant from McKinsey will walk into a DraftKings-esque boardroom someday and show that through ‘proper risk management’ they can get large returns on user loans. The company borrows at 5%, lends it out at (making numbers up here because I’m a simple man) 10%, and pockets the difference plus the house’s take on each wager. But you know what won’t happen? Proper contract enforcement.

As mentioned above, lending out credit for gambling leads to cash flow timing issues or massive credit loss provisions sitting on a balance sheet. The legal process to redress gambling debts is slow and expensive. Not to mention that the user can declare bankruptcy. Meanwhile, the platform has to pay out to the winning side of the bet. This is a financial nightmare. On top of this, DraftKings et al., are legitimate businesses. They don’t have recourse to broken knees. It’s all of the downsides without the risk management practice known as guidos with baseball bats.

Endnotes:

Just Finished: The Grand Strategy of the Roman Empire by Edward Luttwak

Currently Reading: Jacobites by Jacqueline Riding

Up Next: The Bubble Economy by Christopher Wood