Your Start-Up Has A Bad Case of Competition

Your Start-Up Has A Bad Case of Competition

Won't Someone Save Us From the Hockey-Stick Graphs?

Thanks to the proverbial slings and arrows of outrageous fortune, I’ve spent the last 18 months or so working with start-ups. From strategy and finance to operations and product development, I have seen how the sausage is made. While the specific start-ups have ranged from ag-tech to material science, each of them has presented their five-year projections the same way.

On the left-hand side, you see a current loss. The next two years consist of ever-increasing losses until around year 3 or 4 they magically turn profitable and see their operating incomes take off exponentially. Most people refer to this narrative as the ‘hockey stick graph.’

There are a couple of reasons why seemingly every start-up tells this story. The first is that it is the narrative that everyone else is currently telling would-be investors. Therefore, VCs expect to see this graph. If you cannot paint a fancy picture about how their investment is going to the moon, then why would they give you the time of day? VCs know that 99% of start-ups fail, so they are not going to place bets unless there is the possibility of a massive payoff.

The second reason is that the start-up culture has been thoroughly distorted by a handful of axiomatic success stories. Microsoft took off like a rocket in the 1990s, Google did it in the 2000s, and Facebook shot up in the 2010s. The start-up hubris is that every founder asks themselves ‘if they can do it, why can’t we?’ Which is insane. To think this way is to make the categorical mistake of assuming that the exceptions are the rule. But here’s the thing, in start-up land the idea is that in the long run, only the exceptions survive. Thus, a priori one has to act as though they are going to be the exception.

Case in point, one can look to the de facto bible of start-up land – Peter Thiel’s Zero to One. As Thiel accurately notes:

“In the real world outside economic theory, every business is successful exactly to the extent that it does something others cannot. . . Monopoly is the condition of every successful business [italics in original].”1

What sets Facebook, Microsoft, and Google apart is that they enjoy monopoly power. Now, they might not have such power in every aspect of their offerings – for example, Microsoft competes with Amazon in cloud services – but they each have a monopoly in something that funds, either directly or indirectly, the more competition-laden offerings.

The signs of a modern monopoly are:

1. Initial rapid growth

2. Sustained and growing profitability.

We can talk all we want about how market capitalization fits into this but then things get muddled. For example, Airbnb has had rapid growth and a large market capitalization, but it’s not a profitable business yet. It does however have positive cash flows from operations so if it follows the Amazon model it could get there. It’s important to note that Airbnb’s monopoly is not in hospitality bookings but in non-formalized owner-rented hospitality venues.

The important point here is not that magical monopolies exist. The point is that the existence of magical monopolies - who were once start-ups - does not mean that every start-up will become a magical monopoly. Nor that a given industry is likely to be disrupted by a monopolistic start-up.

It would appear that we have equated ‘innovation’ with ‘future monopoly.’ Just because a start-up has a legitimate innovation to offer the market does not mean that the innovation is such that it will send profits soaring to the moon. Instead, if the innovation is imitable and not that different in terms of function and margins relative to existing offerings, then the innovation will face price pressure via competition.

Here it is useful to lift some passages from Ludwig Lachmann who described three forms of entrepreneurs:

“(1) arbitrageurs; (2) speculators; and (3) innovators.

While arbitrageurs make gains from existing price differences, or price-cost differences, speculators as well as innovators hope to make gains from intertemporal price differences or price-cost differences. But while the speculator merely hopes for such differences to come into existence as a result of developments over which he has no control (e.g. changes in demand or the size of harvests), the innovator hopes to bring about such profitable changes by his own actions...

. . . A speculator who buys stock in the innovator’s company helps the latter, but one who buys stock in a business competing with his will help to reduce profits...

. . . If our innovator is pursued by a host of imitators ready to take evasive action into product variation, and if these imitators are, then, surrounded by swarms of speculators, very little can be said about the outcome of the market process.[italics in original]”2

What Lachmann is getting at is that innovation does not occur in a vacuum. More often than not, innovation, if potentially lucrative, is mimicked and profits - if there ever were any - are quickly reduced via price pressure. The real kicker is that the speculators of modern start-up land are the VCs.

From a financial point of view, VCs have two jobs. First and foremost, they are supposed to identify start-ups that have an overwhelming potential of becoming monopolies. Barring that, VCs are meant to look around at the start-ups that their competitors have funded and then invest in similar start-ups in the hopes of (1) stopping their rivals from realizing immense ROI via monopolies, and (2) siphoning off a piece of the profits available in the space. In short, VCs either get lucky or promote competition, which, in and of itself drives their rates of return down. Sometimes they get a Facebook, but more often than not they end up backing yet another shitty scooter company.

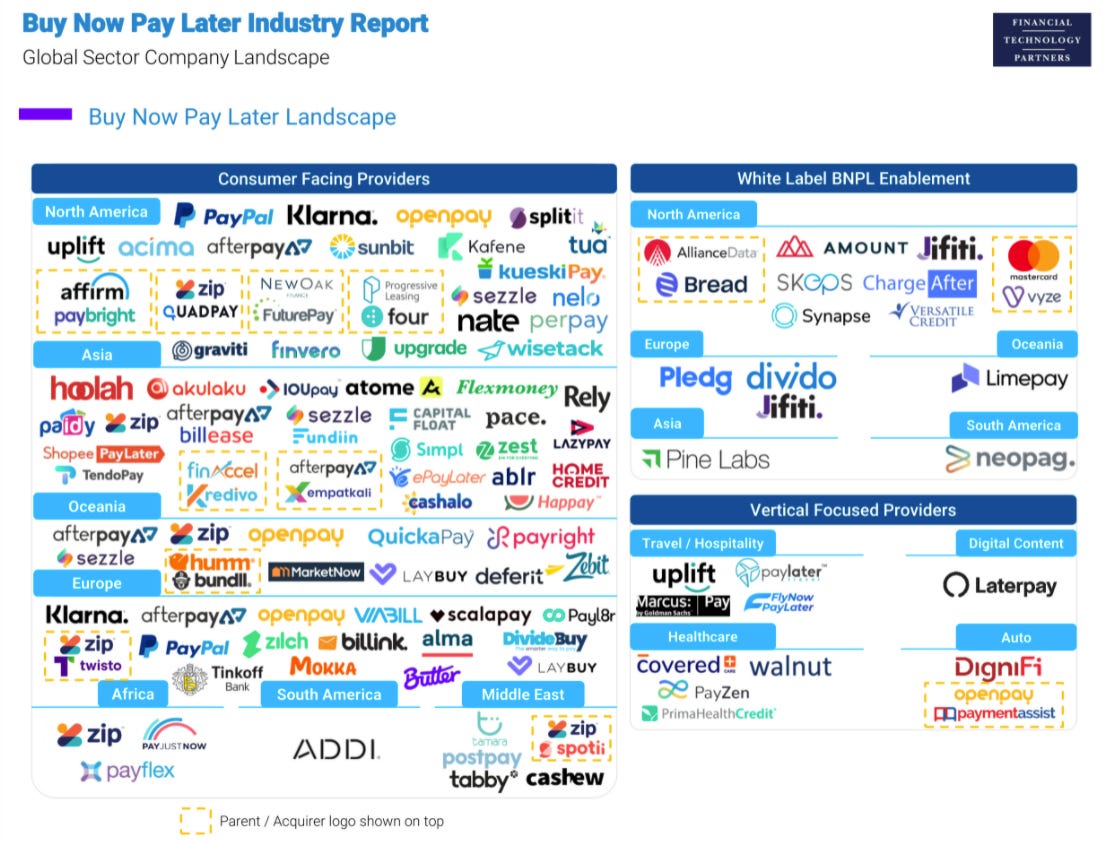

What got me thinking about this topic is that this week I saw that Ron Shevlin - Hi Ron - retweeted a market research report on the ‘Buy Now, Pay Later’ (BNPL) side of FinTech from Financial Technology Partners. The report is well done. Go those guys. Three cheers for market research.

What stood out to me though was this slide.

Now, I’m willing to let folks tell me about how each of these firms is different than the others in some minor way, but can we imagine as true to a significant extent? Is competition non-existent here? No. Then one would imagine that there’s a bit of price pressure going on here.

The authors of the research note six publicly-traded BNPL companies. These firms are:

1. Affirm

2. After Pay

3. Zip

4. Open Pay

5. Sezzle

6. Split it

Collectively, each of these firms has negative net incomes, and all but one - Zip - have negative cash flows from operations. These firms make short-term loans. It’s not a money-printing machine, and barring a few notable exceptions, it has never been a wildly profitable business. Think of who needs BNPL services? It ain’t folks with fantastic credit. As I’ve written before about Affirm:

“Affirm is not in a sexy business. Yea, they have a nice-looking website, but when you peel back the marketing it’s obvious that they’re making what are likely sub-prime loans. Why? Because who needs their product? People who can’t afford to purchase goods upfront. And who are those people? People who do not have money lying around with which to make discretionary purchases. Or in layman’s terms, poor people. Sorry, but if you need Affirm to purchase a Peloton then your fat ass does not need a Peloton. What you need is some restraint. Run outside as I do for the low, low cost of free. God made you a gym, go use it. Seriously, any business that requires its customers to pay up to 30% interest when the S&P 500 returns about 6% is not a high street business.”3

The thing is that in my previous writings I never dealt with competition amongst firms like Affirm. Affirm’s selling point to investors is that its technology allows it to provide the same service - BNPL - for less cost than traditional providers of short-term credit (i.e. credit cards). This difference between what Affirm can do and what Visa does, if it is true, is a theoretical source of increased value. But what if there are - looks at the infographic above - a shit load of companies trying to do the same thing? Then the question shifts from ‘can we do it better?’ to ‘can we do it better than everyone else who is also trying to do it better?’

This shift in the raison d’être of a start-up ought to be crucial for investors and brutal for the companies. As soon as competition appears to be more than a splash in the pan, the jig is up. Monopolistic dominance ain’t coming boys. The choo choo train to Facebook territory is no longer scheduling a stop at your station. Yet, seemingly intelligent people will continue to pile their money into the arena. Why? If I had to guess, I’d place the blame on the world’s most meaningless metric - the Total Addressable Market (TAM).

A TAM is meant to indicate the theoretical maximum amount of revenue your start-up has exposure to. This number can be useful if your start-up has a legitimately new product. It’s a useless metric when there are already firms in the market. Take the BNPL example, the research report restates a figure from BNPL company Zip which places the TAM at about $22-trillion dollars. Which is a dogshit number.

First of all, the market for BNPL is nowhere near that number. If we can all agree on the simple premise that BNPL includes credit cards, then all we have to say is that Visa does revenues of around $22-billion. Sure, if we look at the underlying sales from which Visa makes its revenues then the number gets quite a bit larger, but that’s not Visa’s money. Someone else has a claim on that money. So that ain’t part of your market.

Secondly, as is obvious from mentioning Visa, there are already established players in the space. They are not just going to roll over and get boomed by the likes of Affirm. Instead, if the market for the slightly different BNPL products is lucrative enough - which is so far not seen in the performance of new BNPL firms - then established players have all the incentive to ‘featurize’ the differentiating aspects. In short, there is nothing that Affirm can do that Visa can’t do.

So what gives? Why do folks invest billions of dollars in start-ups that face high price pressure? Well, in part it’s because of the $22-trillion figure. In theory, if a firm were to capture one percent of that market that would mean an annual revenue of $220-billion. Or about 10 times that of Visa right now and around what Apple did in 2020. But again, that number is some made-up shit from a third-rate Australian lender. But that’s the figure that VCs see. They don’t care so long as the total is large enough that a tiny market share can generate a historic ROI. And every start-up trots out an outrageous TAM.

As a rule of thumb, if a company tells you that their market is in the trillions, what they are really telling you is that they don’t know what market they’re in.

Interestingly, the earlier one invests in a start-up the less downside one faces from price pressure. For example, let’s say that you have start-up X which has kind of shitty margins but it eventually grows to a size where the valuation comp puts its worth in the hundreds of millions of dollars. If you are the founder and you put in $20,000 back in the day, then you’re probably walking out, post IPO with some legitimate cash. The same goes for the angels and seed funders. Hence why these firms get funded in the first place.

So what, at the end of the day, am I getting at here. Well, that’s simple. It would appear that the governing investment and valuation paradigm in start-up land is that the monopolistic exceptions (Facebook, Microsoft, etc...) are the norm. As such, each start-up goes out thinking that they will conquer the world and the founder will be the next Zuckerberg. However, more often than not, there is strong competition and price pressure. It is a rare firm that can overcome these to win most of the market. Others have to slog it out like normal companies. Start-ups wave away this situation by positing giant TAMs which VCs ‘believe.’ The result is that exceptionally average companies are funded and marketed as the next big thing when in reality, they are nothing more than mediocre companies. Hell, the majority of them are lucky if we can even call them mediocre five years out.

At the end of the day, very few companies escape competition for very long. This fact seems to have been lost out in start-up land. We are a greedy species. Profits beget competition. Some companies can fend off competitors and maintain their margins, but those are the exceptions. It’s about time we all started to realize that 99% of start-ups are ordinary at best and will remain so until proven otherwise.

Peter Thiel with Blake Masters, Zero to One: Notes on Startups, or Hor to Build the Future, (London: Virgin Books, 2014), 34.

Ludwig Lachmann, The Market as an Economic Process, Mercatus Center ed., (Arlington: Mercatus Center, 2020 [1986]), 125-127.