A Victory Lap of Sorts (And Some Notes On Advertising)

A Victory Lap of Sorts (And Some Notes On Advertising)

Long time no see.

To steal from noted poet laureate Marshall Mathers III – Guess who’s back, back again. This jabroni is back, tell a friend.

The GOAT Gloat

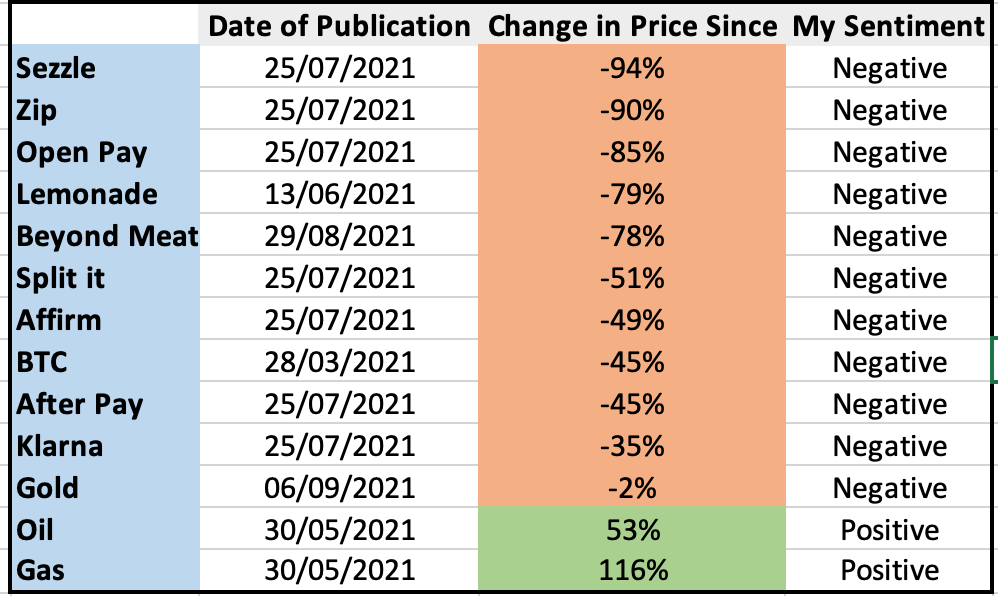

Anyways, let’s ignore pleasantries and updates for now and focus on what’s important. Which is that god damn did I hit some real winners in my writings last year. the following table notes the equities and commodities I name-dropped in 2021, my sentiments thereof, and the movements in price since.

Note that in terms of specifics Oil is for WTI spot, gas is for Henry Hub spot, and Klarna refers to their private market valuation.[1] The specifics might be off by a few bps since I did a very quick search for pricing on or around that date, but the story pans out. As I believe The Ringer’s Mallory Rubin once said of Toto Wolff, I exude excellence.

Did I get lucky? Probably. Most of the Buy Now Pay Later ‘fintech’ firms I went after are Australia-listed which is never a great sign for equity quality, but hey, look at the tape. If you go back and look at the pieces I wrote there are hundreds and thousands of words of analysis laying out why one would have the sentiments I had.

Underlying these sentiments was the simple fact that I live in the real world. I do not get paid to sell equities or commodities. That’s not my book of business. Instead, I have the luxury and sitting back and going ‘what’s the broad framework required for these assets to move in a certain direction, and which of these (downside or upside) makes more sense.’ It ain’t rock science. It just comes down to some level of appreciation about (1) how the world works and (2) what has to happen in order for prices to move a certain way.

I could spend a lot of time talking about those two points but I’ll be brief. At the end of the day, the prices of the equities and commodities I referred to in my pieces reflected prevailing market sentiment about them. Sure we could look at the forward curves on the commodities and see where the market was pricing them but I’m going to go out on a limb and say that the forward prices were below the present spot. The question then is why the market priced the assets in the manner that they did. Put differently, if financial market participants are so god damn smart how come they were so god damn off the mark in the listed assets?

The answer – or at least my hypothesis – is that finance folks are delusional. Full stop. Or rather, they are disconnected from reality in a way that deludes them into holding false conceptions thereof. They (royally speaking here) legitimately thought that the Aussie BNPL firms were worth something. Why? Because there was a narrative and collection of think-pieces that told them that fintech was a gold rush. Which, maybe it is/was. As of writing, Google is telling me that the firm formerly known as Square is up 580% since its IPO. Yet at the same time, it’s down 47% year-to-date.

My personal favorite dumpster fire of cash incineration is the vertical farming/greenhouse sector where dumb fucks like the folks at AppHarvest are down 70% since their SPAC debut. Not to mention the garbage palace that is Kalera AS which is also down 72% since its inception. But that whole sector exists because of a misunderstanding of the unit economics and macro-environment that runs the agricultural sector. The peak of hubris is believing that an industry composed of the likes of John Deere (up 2% YTD), Bayer (up 40% YTD), and Tyson (flat YTD) is run by idiots awaiting their inevitable disruption. Agriculture is a cutthroat volume business that requires actual physical capital not just a leasing agreement from AWS and some code.

I should note that I was also bearish on the Canadian real estate market. My bearishness came from an expectation that when rates went up that shit would hit the fan. Given that the central banks risk-free rate has now tripled so far this year I’ll just leave this context here:

Oh, yea, and one more thing (I promise I will stop the ‘I told you so’ in the next paragraph). I had a chat with some metals and mining investment bankers this time last year and their core question was ‘what metal is the one to watch in the near to medium term?’ I said, copper. Why? Because whether the future looks more like the present or a green utopia, you’re going to need copper for infrastructure projects (looking at you sub-Saharan Africa) and mine projects just aren’t moving fast enough. They laughed and went on about gold. So tickle me surprised when this dropped (note: I still believe Joe Weisenthal to be the personification of an undercooked potato):

Everything You Need to Know About Advertising

Moving on though because frankly, no one cares for gloating. Let’s talk about advertising. Why? because allegedly I’m a media-tech executive. Which is a weird thing to say because I’ve never had any interest in the space. But hey, it’s a lucrative industry if you play your cards right.

Advertising has got to be one of the most misunderstood industries out there. I’m not talking about misunderstandings from those on the outside looking in but rather amongst those inside the industrial citadel. Although to be fair, those on the outside are oblivious to the reality at hand.

What is advertising? I don’t mean this in some philosophical mumbo jumbo that marketing profs spew in order to validate their existences. I’m talking brass tax. What is advertising? It is merely the connection between an advertiser and their target audience. That’s it. It’s not witchcraft. It’s not voodoo. It sure as shit is not the genius of Don Draper. It is merely the facilitation of connection.

Platforms – otherwise known as media – exist to facilitate the connection. Once you understand this the whole façade and opacity of advertising high tails its way out of your mind. Think of a local newspaper. The price you pay for it is not to fund the journalists. Instead, it is to cover the physical or digital delivery costs of the content. The journalists ought to be paid solely by the advertisements in the paper. Their job is to create content that will drive eyes to sections of the paper wherein an ad sits. That’s it. It’s not to ‘tell the truth’ and break big stories. Let alone ‘inform the electorate.’ It is merely to pull eyeballs towards a creative asset.

There are exceptions to the rule when it comes to newspapers in particular. Think of the New York Times, Wall Street Journal, and Washington Post. Those papers are largely subscription-driven whereby the readers are actually paying for the content. Sure, there may be advertisements but those are the cherry on top of the content-revenue sundae. For everyone else though, journalism is merely filler to persuade eyeballs to look at or near an ad.

Shifting gears, think about Facebook for a second. What business is Facebook in? It’s an advertising platform. Simple as that. All the social networking functions are meant to get people to scroll and click through enough pages to see a certain amount of advertisements along the way. The revenue function for Facebook (I’m refusing to call it Meta because, well, it’s a stupid name) is:

Revenue = f(eyeballs, time on screen, frequency of ad placements, value of engagement)

The genius of social networks is that organic user-generated content fills pages in which ads are placed. Facebook does not have to make anything to go around them. It’s as if newspapers were filled with volunteer submitted pieces. The best part is that the content creators are the target audience themselves so we make the content that then directs our eyes to advertisements aimed at us.

In terms of unit economics advertising is about arbitrage. There is a price that an advertiser is willing to pay for an ‘engagement’ which might be an impression, a click, or some other KPI. There is then the cost of generating that engagement. A successful platform does the latter for less than the former. In the case of Facebook, we can write a profit function as:

Profit = Value of engagement to an advertiser – Cost of engagement acquisition

The cost declines as the effectiveness, or pull, of content rises. Who knows what content you want to see the most? Your friends. In turn, your friends are incentivized to post content thanks to social gratification gained via likes, shares, and comments. It’s a rather ingenious business model. Until people get bored of Facebook, Instagram, etc...

From a policy point of view, you can see pretty clearly that Facebook et al. are media companies. They provide the medium through which advertisers are connected to their target audience. Yes, they don’t make content but they facilitate the creation of content because that’s what drives their advertising business model. In the same way, you can say that USA Today is not in the business of content creation. Instead, they are in the business of connecting advertisers to their audience with content dispersed around ads. Journalists are little more than influencers being compensated for their writing of something to go around the ads. Journalists get cash, Facebook users get the opportunity for social gratification. It’s not that different and anyone who tells you otherwise is a mollusk of an adult.

As a final note, I would like to point out that much of B2B advertising is junk. Especially trade journals. Let’s imagine an aviation industry journal. Within its pages are ads for Boeing, Airbus, and whatever aviation service companies exist. The journal is distributed for free to the target audience and is fully ad-supported.

Now ask yourself, is the CEO of Delta – Ed Bastian – going to see an ad for an Airbus A360 and go ‘shit, gotta have that as opposed to the Boeing competitor’? No. Because there are more important factors. In fact, the ad doesn’t even help raise awareness because Eddy knows about Airbus. They probably call him every day. So why do the ad and the trade journal exist?

Well, it’s because companies get it into their minds that advertising works in the B2B space. To be fair, it can work, but I’d wager that 98% of B2B sales consist of relationships between buyers and sellers. The ads merely bring a ‘vibe’ to a company. It’s a way of saying ‘hey, look at us, we’re so cool and legit that we can have an entire marketing campaign around hemorrhoid cream.’

If a firm is large enough, the cost of marketing appears relatively small and sales happen which creates the sense that the ads did something to facilitate them. But it is bullshit. Or at the very least, B2B marketing – especially at the high end of sale size – has a neutral to negative ROI. Better to hire a schmoozer with connections than an MBA focused on Google Analytics traffic within a programmatic environment.

Let’s call it a day shall we? I don’t know if there will be more posts going forward but for the time being, let’s say that there will be.

[1] https://www.bloomberg.com/news/articles/2022-05-19/klarna-seeks-new-funding-at-lower-30-billion-valuation