Have We Lost the Plot?

Have We Lost the Plot?

Real Estate and the Decline of Canadian Economic Dynamism

Gore Vidal famously quipped that ‘USA’ stands for ‘The United States of Amnesia’ in that seemingly no one in the Land of the Free knew much of anything about what happened prior to their own birth.1 For Vidal, it was not that folks were denied opportunities to learn about their nation’s history, but rather that no one felt a need to learn anything outside of their own existing corpus of knowledge. While Vidal was certainly right about the United States, in particular, his view also holds for Canada. Put bluntly, next to no one knows anything about the land Voltaire referred to as “a few acres of snow.”2

The reason why we ought to bemoan this situation is not that there is some sort of infinite wisdom to be gleaned from the past, but rather, a nation’s past says something about the nature of the nation as it stands today. Now, this is not a political essay. Rather, my intention is to talk about Canada’s economy and how we have collectively decided to ignore our situatedness within the global economy.

To begin with, let’s take an unorthodox approach. Right now I have my LinkedIn account open to the ‘Jobs’ tab. For those who are unaware – or happily oblivious due to comfortable employment – the ‘Jobs’ tab is where LinkedIn aggregates job posting based on general terms that you – the user – select. For me, the jobs that show up are overwhelmingly for finance and located across the country. Categorically, the job-posting entities fall into three buckets: The Big 5 Banks, Pension Funds, and Real Estate Developers/Lenders. Perhaps as little as 1/10th of the postings focus on firms in the ‘real economy’ (i.e. companies that build things other than real estate). This situation may seem perfectly benign to many but I read it as a dire situation for all of us living in Her Majesty’s northern domains.

You see, in order to economically compete, individuals, firms, and countries have to play to their strengths. In other words, ‘what is it that I/we do better than almost anyone else?’ The problem here is that we are not better than everyone else at real estate, banking, or pensions. And, even if we were, only banking would matter since real estate is the definition of a non-exporting field and pension funds only matter if you’re one of the pensioners – here’s looking at you Ontario Teachers. If we are the best in the world at industries that do not bring global capital to the broader population then there really is no point since all we would be doing is robbing Peter to pay Paul. Furthermore, if foreign capital tends to flow into a particular sector then one has to ponder the motivation thereof. (Spoiler alert: in 2018, the BC Government commissioned a report on the effects of money laundering - both foreign and domestic on the province’s real estate market).

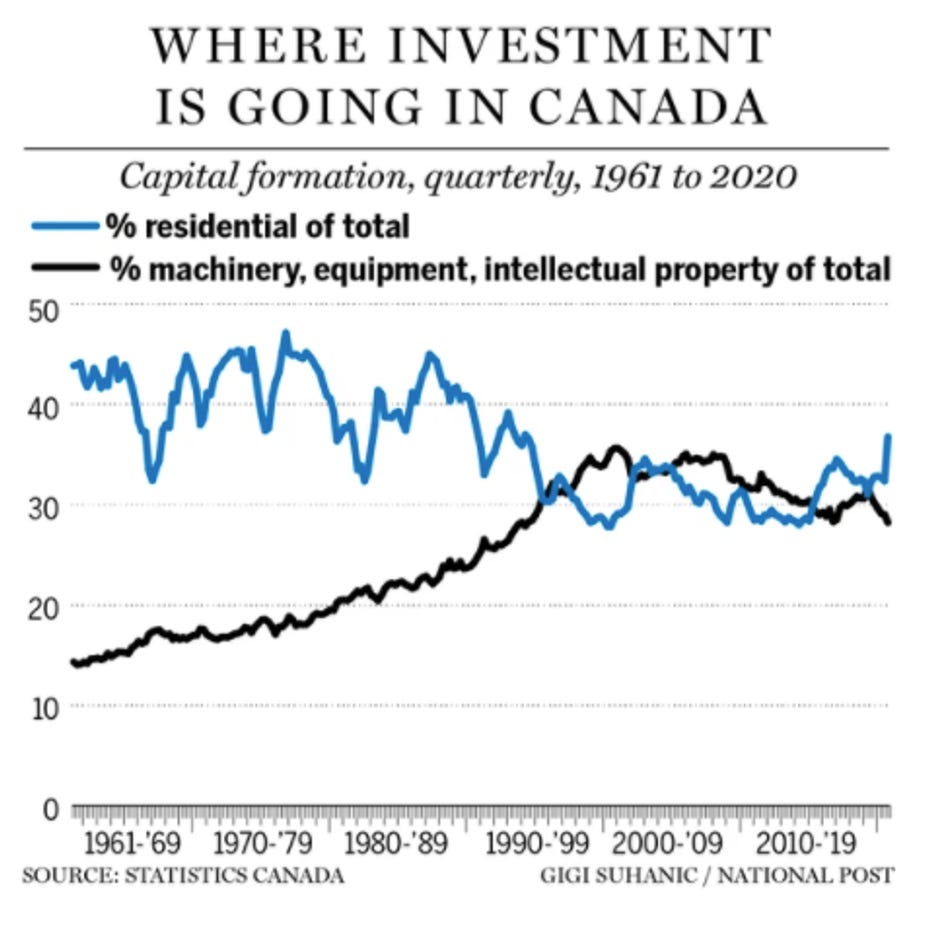

While banking and pension funds are what they are, I want to ignore them – much like how they ignore my job applications. Instead, let’s focus on real estate. Why? Because real estate is seemingly our leading industry in Canada in terms of collective growth. For context, Statista tells me that real estate is actually our largest industry in terms of GDP contribution. In 2021, the residential component of the sector itself accounted for 37% of overall investment in Canada.3 More concerningly, as of 2018 real estate accounted for 76% of Canada’s wealth.4 That’s right, over three-quarters of our collective wealth consists of homes, condo towers, and office spires. Thus it is no surprise to me that every day I get notifications from LinkedIn telling me how the likes of Cadillac Fairview, Rio Can, Triovest, and Brookfield are looking for real estate investment analysts. By comparison, our national investment in PP&E and IP has slowed since the 1990s as shown in the figure below.5

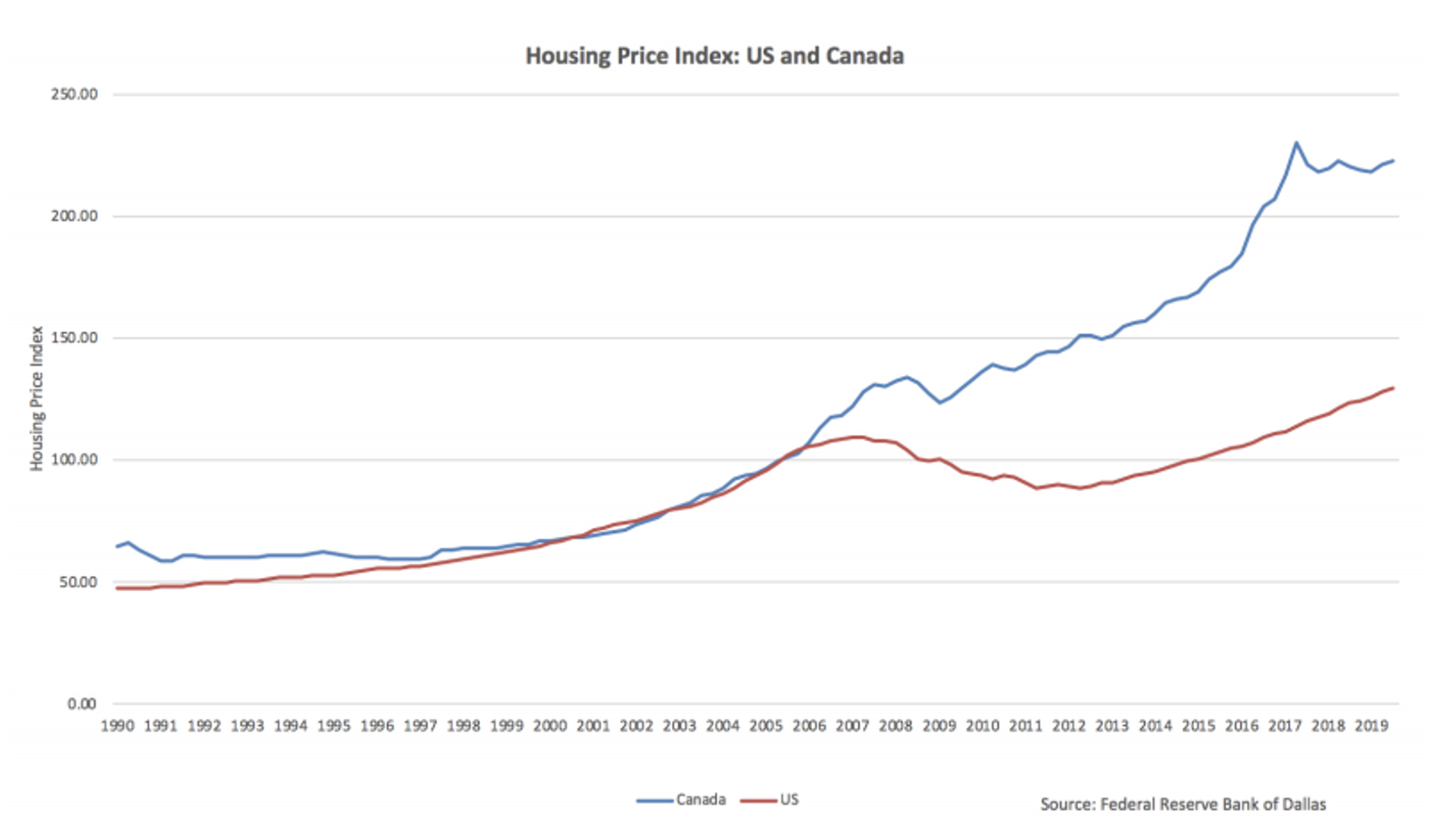

All of this investment in real estate might be okay if it weren’t for the fact that there is clearly a bubble going on as opposed to cash flowing in response to past underinvestment. What evidence is there of such a bubble? Well, first of all, there is the fact that this phenomenon is so obvious that it has its own Wikipedia page. Secondly, there are the ever-increasing reasons for believing it to be a bubble as espoused by the likes of North Cove Advisors’ Ben Rabidoux and Steve Eisman of The Big Short Fame. Lastly, there are time-series data such as the following from an MIT thesis by Shirley Zhou on the Canadian Property Boom:6

Now, again, a boom is a boom is a boom. But the issue here is that this boom is a bubble. Which, is okay in the realm of Beanie Babies, NFTs, and fake Da Vinci’s, but not when it’s an asset class that makes up over 75% of a nation’s wealth. A 10% reduction in real estate prices nationwide would mean a decline in national wealth of nearly $1-trillion.7 Which, to me, seems like a big ‘oof’ moment. But the matter is worse than just the potential for a one-time decline in nominal value.

For anyone who went to business school, or who has a shred of worldly knowledge, it is standard practice to assume that if a company’s liabilities exceed its assets then it is bankrupt insofar as it should be in a state of illiquidity or insolvency. However, in reality, this is not the case. There is another possibility in which a firm can be bankrupt from the point of view of the balance sheet yet still a functioning entity. When this occurs on a broad basis, the ensuing economic downturn is called a Balance Sheet Recession as coined by Nomura’s Richard Koo. Long story short, what happens is that a firm used debt to purchase assets that unexpectedly declined in value to the point where the underlying assets became less valuable than the outstanding liabilities yet still generates enough cash to cover debt servicing.

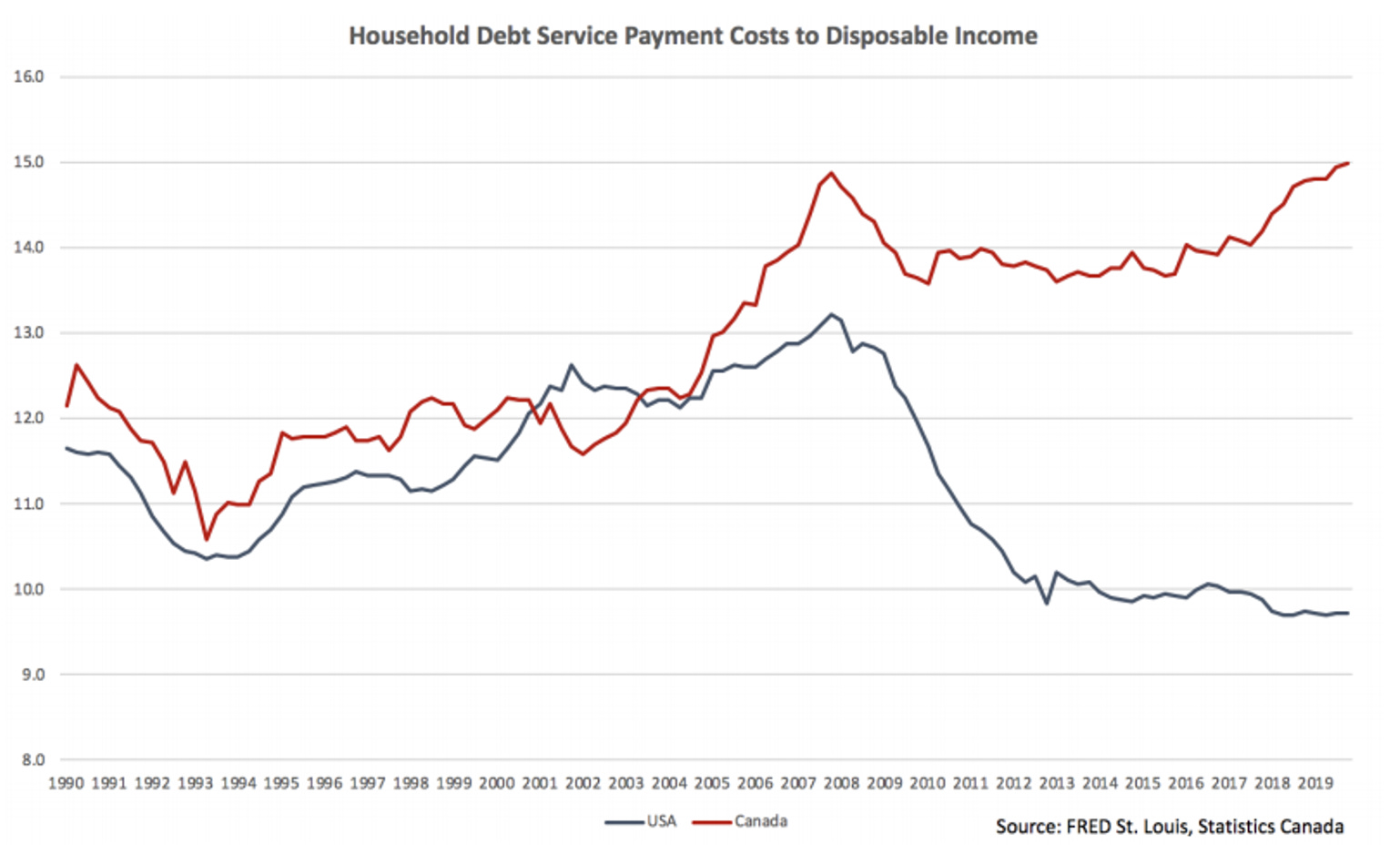

The reason why a firm is not actually bankrupted by this situation is that they might have cashflow generating assets and operations which can cover the costs of debt financing going forward. If you are the CEO of a firm in this situation, shit looks less than ideal but not terrible. The reason is that if you stick it out and pay down the debt going forward, then the equity of the shareholders is not wiped out while creditors are happy as long as the cheques keep clearing. In fact, for the creditors, this is an okay situation since if they let the firm keep paying their debt fees, then they will someday recuperate all the expected cash flows while if they were to foreclose on the assets, they would take a hit themselves since the assets are now worth less than the loan balance. Problematically, though, this means that the firm is not going to grow much going forward because debt servicing costs now take up a sizable chunk of the firm’s free cash flow and the bulk of existing assets cannot be used as collateral for further loans. Do you see the problem here in terms of Canada? Because Koo did back in 2015. If you’re not quite sure what I’m getting at, look at the following chart from Zhou:8

In general, Canadians are spending increasing amounts of their disposable incomes on servicing debts that are overwhelmingly mortgages whereas our American neighbors learned their lesson from the Sub-Prime Mortgage Crisis.

As long as property prices keep rising, then everything is okay for now because you can always sell the asset (the building) to cover the mortgage. But, and this is a big but, if the asset value declines then you can’t use that get out of jail free card. You wind up in a situation where if you are highly levered on your mortgage then when it goes underwater – mortgage balance exceeds property value – then you cannot leave your property without taking a major hit which will be due upfront since the bank will no longer have recourse to the asset as collateral.

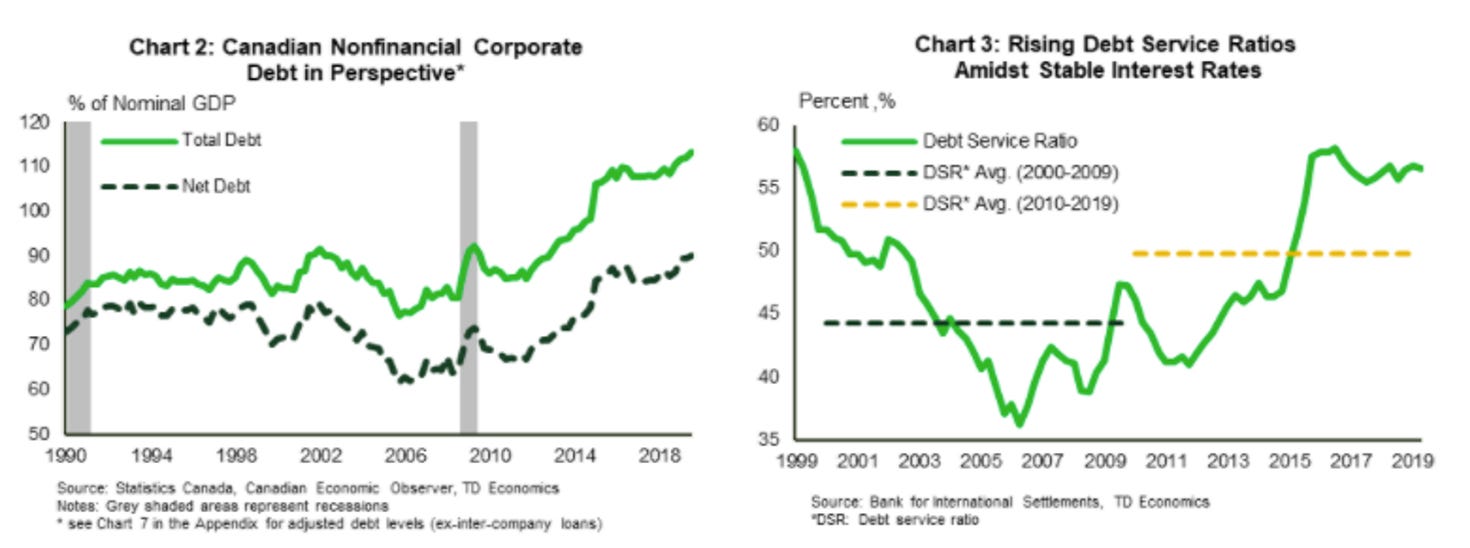

The question then is, how many Canadians – homeowners and commercial property owners – would be able to sell their property at a loss given existing debt commitments? Probably not all that many given that household debt is currently at 111% of GDP while the following figure from TD show the situation for corporates:

The knock-on effect of this is that the housing market would freeze up. No one – speaking hyperbolically here – would be able to take a hit, so the existing housing stock would decreasingly serve as a source of inventory. Given that prices are falling you would expect young people and first-time homeowners to step into the space except that there will be reduced inventory stock due to reluctant sellers and less incentivized builders and mortgage lenders. Which is a fancy way of saying that real estate – our current driver of economic activity and wealth generation – will go the way of the dodo while everyone pays off their debt. A.K.A, a housing crisis.

This situation would not be the case in the United States since a good deal of those folks have access to 30-year fixed-rate mortgages. Meanwhile, up here in the snow-covered acres conservative individual borrowers sign up for 5-year fixed rates. Thus, sooner, rather than later, one would have to pay the piper in terms of adjusted debt servicing costs.

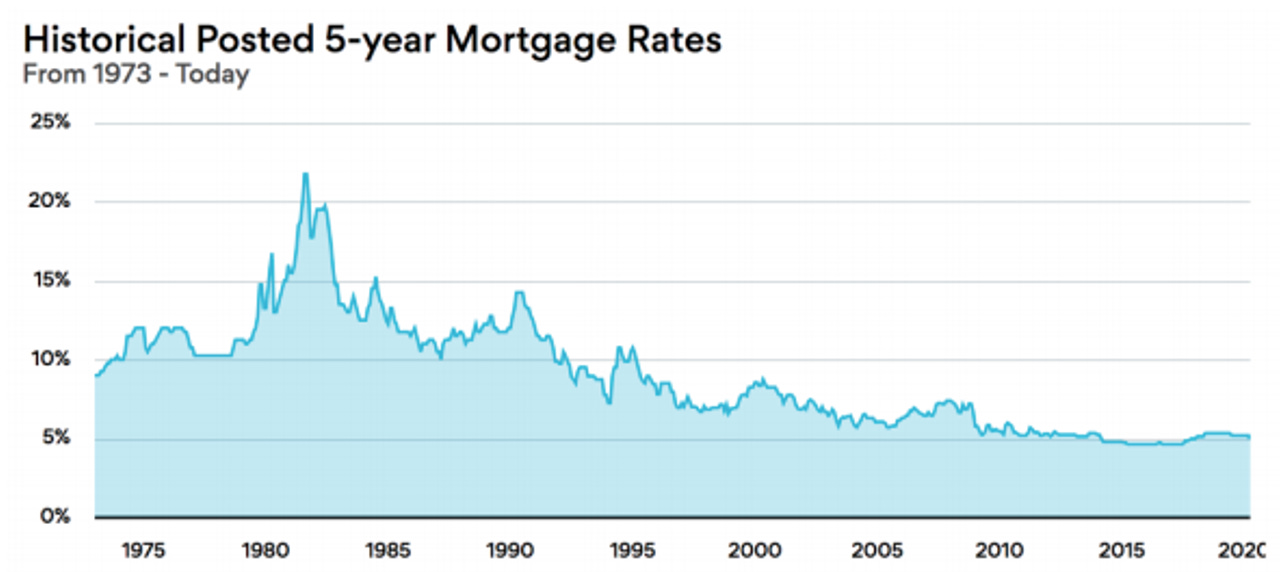

The reason why we do not sit around worrying about rising rates or asset price declines is that we are living in the middle of a forty-year slide in lending rates in Canada, for example, the following is the typical 5-year mortgage rate since the early 1970s.9

We are simply of the mind that interest rates are naturally low and tend to decline over the long run. This is one hell of an assumption. As any indebted Canadian – such as yours truly will tell you – much of our debts are not fixed rate. For example, I’m sitting on a student line of credit from one of the Big 5 banks that is pegged to the prime rate. This situation is okay for now because prime is at a record low, but as soon as rates rise, so do our payments. For example, right now, CIBC has a prime rate of 2.45% which is the lowest on record since at least 1974. For context, the record high was in 1981 when the prime rate hit 22.25%. Based on simple math, if prime were to rise by just 0.5% then my monthly payments are going to jump by 20%. My debt load is relatively low, but how many folks out there can handle a 20% increase in debt servicing costs overnight?

So, what the hell does this have to do with history as proclaimed at this essay’s opening? Well, I’m glad you asked. You see, there was this Canadian historian in the early-to-mid 20th century named Harold Innis. Professor Innis had this theory that others refer to as the “staple thesis.” In this thesis:

“a staple represented a leading, primary resource export commodity, around which settlement systems, institutions, and transportation networks developed. As the key driver of economic development, the staple dominated political and economic life, linked peripheries and metropolitan markets, and structured future economic prospects.”10

This take on national economic development shows itself in two of Innis’ seminal works entitled The Fur Trade in Canada and The Cod Fisheries. Without getting too much into the details, the summary of an Innisian worldview is that for economies like Canada the key to development and economic activity is the leveraging of commodities. In leveraging these, the nation itself takes on a particular shape and structure ranging from settlement locations to laws and educational foci.

To make it blunt, Canada is not a service economy. Or, at least we are not a world-leading one. If you are a world-class organization looking for financial services or consulting work then you do not go to Toronto. Instead, you waddle off to London, New York, Munich, Geneva, or the likes. The same goes for industries like engineering, technology, and health care. We are simply middling when it comes to being smarter than everyone else. Yes, we can beat the likes of Denmark(?) but that does not make us world leaders.

What we can outperform the rest of the world in are natural resources. Hence why our collective economic development has historically consisted of staples such as fur, cod, lumber, metals, and hydrocarbons. But yet, our current economic growth narrative does not consist of staples. Instead, it’s god damn real estate. Walk into a school of business or grade 12 classroom and ask how many people are planning to work in metals, forestry, oil, or related industries such as railroads. I’m willing to bet that you will not get many hands – except in Alberta of course. Instead, folks are looking to work in technology and finance which in turn learns to them likely ending up in some form of construction, real estate, or industry that cater to those who do.

This is why I am bearish about the Canadian economy. We simply do not understand our economic reality. Instead, what we are doing is betting it all on red in the form of real estate as funded by our oligarchic banking system that is explicitly and implicitly backed by the Canadian government. For a variety of factors, it is no longer deemed legitimate or cool to extract natural resources, yet, we are not well situated or equipped to do anything else. Try telling folks outside the Waterloo-Toronto-Quebec City corridor that they are now going to work in technology and/or the financing of condo towers and they will gesture to the nearby woods and say ‘yea, totally, because that makes fucking sense.’ Rather than foreshadowing a new era of economic development, our economic obsession with real estate belies an underlying stagnation in which we are all standing around with no idea what to do now that resources seem off the table.

Title directly inspired by chapter 2 in Rick Nason, Rethinking Risk Management: Critically Examining Old Ideas and New Concepts, (New York: Business Expert Press, 2017).

Voltaire, Candide: Or Optimism, trans. Theo Cuffe, (New York: Penguin, [1759]), 69.

Kevin Carmichael, “While the world is in the midst of a tech revolution, Canadians bet on real estate,” Financial Post, 1 February 2021: https://financialpost.com/news/economy/while-the-world-is-in-the-midst-of-a-tech-revolution-canadians-bet-on-real-estate

Jesse Ferreras, “76% of Canada’s national wealth is wrapped up in real estate, and the market is slowing: data,” Global News, 19 December 2018: https://globalnews.ca/news/4775685/canada-national-wealth-real-estate/

Ibid.

Shirley Xueer Zhou, “A Study of the Canadian Housing Boom,” Master’s Thesis, (Cambridge: MIT, 2020), 11: https://dspace.mit.edu/bitstream/handle/1721.1/127000/1191228521-MIT.pdf?sequence=1&isAllowed=y

Using Q4 2020 data from: https://www150.statcan.gc.ca/n1/daily-quotidien/210312/dq210312b-eng.htm

“A Study of the Canadian Housing Boom,” 12.

Ibid, 16.

Matthew Evenden, ‘Introduction’ in Essays in Canadian Economic History: Harold A. Innis, ed. Mary Innis, (Toronto: University of Toronto Press, 2017 [1956]), vi.