Between Professors and Practitioners

The Difference Between Being in the Weeds and Studying Them From Afar

On September 14th, the historian Adam Tooze did a Twitter spaces conversation with the Financial Times’ Alphaville team in support of his new book Shutdown. Now, I have to pay rent so I didn’t tune into the conversation – ya know, work and all – but I was aware that it occurred. So color me surprised when this week Professor Tooze got into a Twitter spat with the editor of Alphaville Izabella Kaminska.

The affair began with Tooze tweeting the following in response to Alphaville running a piece by Kaminska based on a conversation with Oil and Gas financier and advisor Phillip Lambert’s.

Now, I’m not going to lay out the dozen or so responses and replies between the two but the gist is that Tooze thinks that Lambert is out to lunch and talking his own book while Kaminska believes that Lambert has a reasonably valid viewpoint. What shocks me – a mere simpleton – here is that Lambert’s take riled up someone such as Tooze to the degree that it did. Now, you can’t read tone in a tweet so perhaps I’m wrong as can be here, but Tooze’s apparent shock and/or frustration seems odd.

Lambert’s position is basically that net-zero efforts will kill investment in natural gas and thus supply will decline prior to similar declines in the demand for such resources. Why? Because if investors – read: institutional investors – decide that they will not allocate capital to exploration and production efforts today then future supply will not actualize. Furthermore, investors will not be interested in funding E&P efforts that ultimately create assets that will be ‘stranded’ in a net-zero environment. For example, as JP Morgan notes in their Annual Energy Paper, under the IEA’s ‘Sustainable Development Scenario’ – which is more chill than the Net Zero 2050 scenario they published a while back – 42% of oil and 26% of natural gas assets would be worthless in only a few decades.

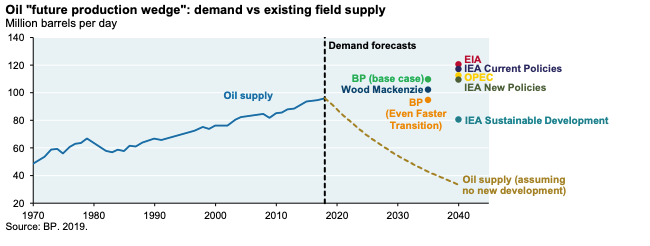

Stepping away from natural gas and looking just at what would happen if oil E&P efforts were to grind to a halt we can see that supply would be 2-3 times below predicted demand by 2040:1

While one may run around claiming that this is all a load of fearmongering – which is, based on the non-Tooze-Kaminska response from economist Daniela Gabor, a common interpretation of Lambert’s position – it does seem like a reasonable concern to have. For example, looking at the sad bastard of North American energy known as Canada, ARC Energy notes that back in 2011 12,827 oil and gas wells were drilled. The forecasted amount for 2021 is 4,247.2

The grain of salt here is that Canada’s oil largely comes from oil sands and that one reasonably assumes that each well drilled today has greater effectiveness and therefore two wells drilled a decade apart might not be fair comparisons, but the fact remains that you cannot simply wave away a 66% decline in drilling activity.

Even though Canadian energy revenue is forecasted to exceed all years in the past decade, drilling activity has not picked up. Instead, firms are paying off debt, doling out dividends, and improving their balance sheets. The expectation is that drilling will take off in the near term, but that’s a hell of an assumption. Again, using ARC’s data, reinvestment in conventional oil and gas in Canada has been on a steady decline of ~50% this decade while oilsands development is down ~66%. Rather than a sunny day of an energy comeback, one could interpret the situation as consisting of established producers resting on their cash-flow generating laurels as institutional investors ranging from Caisse de dépôt to Warburg Pincus reduce or halt engagement in the oil and gas sector. The moral here is that there is, at a minimum, a shred of validity and reason to Lambert’s position – even if he is hamming it up for the papers.

While this Twitter debacle is – in the grand scheme of things – petty and meaningless, it points to a broader disconnect one finds in the world of financial conversations in which there are two camps. The first is what I call ‘the professors.’ This group consists of literal professors such as Tooze – who haunts the halls of Columbia – but also policymakers, journalists, and general talking heads who are at least one step removed from the industrial realities they speak about and are interested in. The other group is labeled ‘the practitioners’ who more or less deal, or grapple with, the functional realities of industry. Often the difference between the two is that the first group will speak broadly about a topic as though it consists of Platonic ideas while the second can tell you about the unit economics of production.

As an example from my own life. For those who don’t know – which is almost everyone – I pay my rent in part by doing some work in the space of Ag-Tech and the ‘future of farming.’ Basically, I do research and build models around investment theses tied to things like harvest automation, next-gen greenhouses, and vertical farming. I’m no expert here, but I do good shit. Anyways, I focus on the unit economics of production. For example, how much does a strawberry cost to grow? In this sense, I’m a practitioner. While my world consists largely of going ‘yea, vertical farming is a niche, high-end, side hobby’ professorial folks at places like Bloomberg, CNBC, or, closer to home, The Globe and Mail would have you think that it’s the next big gold rush. Why do they think this way? By cynical view is that it is because they buy the hype. More realistically though, their distance from the matter means that they can adopt paradigms that make sense in their professional circles but which are ludicrous in the face of reality.

It is not my intention to insist that practitioners and professors are mutually exclusive and collective exhaustive groupings. There is obviously quite a bit of bleed between the two and grey dominates the scale between black and white. Indeed, sometimes – especially when the paycheques start coming from new sources or political winds shift – you see someone move from one team to the other.

Case in point, one can look at the career of Mark Carney. Back when Carney was partially responsible for the Canadian economy he was quite adept at pointing out that resource development in Canada was a good thing and, in fact, advocated that the country ought to “improve [its] exposure to countries driving the commodity cycle” which would mean increased resource – oil, gas, metals, and lumber – extraction.3 Now that he’s the well-compensated “Head of Transition Investing” at Brookfield, and liked more by the Liberal Party than the Conservatives, he’s suddenly Mr. Climate Change.4

Before you say that Carney’s opinion changed when the facts did, let me remind you that low-brow adolescent schmucks like me were more than aware of climate risks back in the golden days of 2006 when Mr. Gore rode the scissor lift to show off a graph.

But what does the difference in viewpoint and approach mean in practice? To my eyes, it is not so much that the professors are wrong and the practitioners are right but rather that they arrive at similar conclusions in differing ways at different times. I’m willing to wager that sometimes the professors beat the practitioners to the punch. My gut tells me though that the practitioners, the ones living their lives in the weeds of the matter, probably get to the punchline before the professors even start telling the joke. This seems highly likely – and somewhat obvious – in the case of finance. Time for a bit of a case study.

For this, let’s use a literal practitioner and a literal professor. On the practitioner side, we have everyone’s favorite hedge fund manager-turned-conspiracy theory bogeyman George Soros while on the professorial side we have Pepperdine University’s, Jason Blakely. Last year Blakely published a work entitled We Built Reality: How Social Science Infiltrated Culture, Politics, and Power with Oxford University Press. As a piece of scholarship, it’s alright. It’s one of those works that a freshman would read and suddenly think that they knew everything. As a piece of intellectual history, it’s uh, a little bareboned. Again, I’m just a schmuck, but I’d argue that my 8 pages on the development and implications of the Efficient Markets Hypothesis in this paper, does a better job than Blakely’s 21-page chapter on “Our Free-Market Scientists.” Anyways, back to the matter at hand.

Blakely’s thesis is that social scientists believe that they conduct “research akin to that in the natural sciences” when in reality social scientists create paradigms and meanings that, if adopted by the powers that be, create the very scenarios that the researchers claimed already existed.5 Basically, the idea is that if you think that markets are efficient, then you will create models and enact behaviors as though that hypothesis was true. A consequence of this phenomenon in Blakely’s mind is that this procedure can often lead to failures when reality rears its head.

One could look to the failure of the BSM-option pricing model in 1987 as an example of a world created assuming the correctness of a theory which was then proven false by the facts of reality – although it took a few years to be disproved.

One of the social science theories that Blakely takes issue with is that of the free market as a spontaneous machine that regulates itself and optimizes the allocation of capital. As he notes:6

“To those who believed in the technical [seemingly scientific] models underlying the simplified [machine] metaphor, such outcomes [i.e. market crashes] were excluded by a highly rigorous science that made certain idealized assumptions about human rationality. The idealized models predictably showed that such things could not occur. In this way, a certain strain of popular economic authority made it difficult for many people to imagine the very phenomenon that this mode of thinking helped spawn.”

If your eyes glazed over reading that bit, allow me to summarize. In Blakely’s mind, the idea that markets are the most efficient means of resource allocation – a fine-tuned machine in the metaphor – led to the inability of those in power to imagine a world where freer financial markets could lead to market busts such as we saw in 1987, 2001, and 2007/8.

In general, I’d recommend Blakely’s book to most people. However, in this work, he suffers from the professorial pitfall of – to be blunt – not getting into the weeds of the matter. Or rather, Blakely knows just enough to sound smart on a topic as compared to the average Joe – or a labradoodle.

You see, Blakely is very close to being correct in a meaningful manner. Did politicians, regulators, lobbyists, and industry talking heads make assumptions about the nature of markets that in turn shaped the markets themselves? Yes, this seems undeniable. For example, in his work, An Engine, Not a Camera, Donald MacKenzie notes how Milton Friedman lent his voice to the Chicago Mercantile Exchange’s efforts to legalize non-agricultural option trading via alleged economic theory.7 But what Blakely ignores is that people within the financial industry, and even the economics profession, were fully aware that the efficient, market-as-a-machine, view was dog shit.

Checking the index to Blakely’s work, one notes the absence of two names: Lavoie and Soros. I will be moving on to Soros’ work in a moment but first let’s just point out that in the 1980s, Austrian economist – as in the school of thought, not the nationality – Don Lavoie was denouncing the view of economics as science per se from within the econ faculty. As G.B. Madison summarizes, in Lavoie’s view:8

“There is nothing wrong, per se, with abstract, purely theoretical constructs like homo economicus, general equilibrium, Paretian optimality, rational expectations theory, or the efficient-market hypothesis, but there is, nevertheless, an inherent danger associated with them. This is the danger of mistaking theoretical attractiveness for practical relevance, of, in a word, forgetting, that constructs such as these are, indeed, constructs, that is interpretations, and not objective representations (‘pictures’) of reality itself.”

As Lavoie said himself:9

“[economics] is not so much a non-interpretive science as it is an interpretive one that has been striving to be otherwise in spite of itself.”

One should note that Lavoie was far more of a free-markets individual than the likes of Milton Friedman, yet here he is, seemingly siding with Blakely. But alas, this is more of a critique of Blakely’s pre-writing literature review than anything else so let’s hop over to Soros.

Also writing in the 1980s, Soros put forth his theory of reflexivity in his work The Alchemy of Finance. Early on in the work, Soros comes out swinging against the economic paradigm of efficient markets by positing that “the concept of an equilibrium seems irrelevant at best and misleading at worst.”10 Even more brazenly, the Hungarian behemoth proclaimed that “I do not accept the proposition that stock prices are a passive reflection of underlying values, nor do I accept the proposition that the reflecting tends to correspond to the underlying value.”11 Instead, Soros posited that “stock prices are determined by two factors – underlying trend and prevailing bias – both of which are, in turn, influenced by stock prices.”12 These factors reflexively alter themselves in response to the other. Rather than equilibrium or intrinsic value one faces an ongoing evolution based on subjective parameters.

Soros notes that while his theory of reflexivity paints a narrative pattern of expected price movements that seems to jive with reality most market participants do not adopt his views. Why you might ask? “Part of the answer must be that market participants have been misguided by a different theoretical construction, one derived from classical economics, and even more important[ly], from the natural sciences.”13 Sound familiar? Towards the end of the work Soros really does eat Blakely’s lunch by stating:14

“People participate in science with a variety of motivations. For present purposes we may distinguish between two main objectives: the pursuit of truth and the pursuit of what we may call ‘operational success.’ In natural science, the two objectives coincide: true statements work better than false ones. Not so in the social sciences: false ideas may be effective because of their influence on people’s behavior and, conversely, the fact that a theory or prediction works does not provide conclusive evidence of its validity.”

As a real kick in the pants allow me to quote both Soros and Blakely at length for a moment. First Soros, and then Blakely:15 16

“. . . people in the academic professions are not so lucky: they compete directly with natural scientists for status and funds. Natural science has been able to produce universally valid generalizations and unconditional predictions. In the absence of a convention to the contrary, social scientists are under great pressure to come up with similar results. That is why they produce so many scientific-looking formulas. Declaring social science a false metaphor would liberate them from having to imitate science. [note the use of the word metaphor in a previous Blakely excerpt]”

“By the late twentieth century the new, more mathematically rigorous, and ahistorical form of economics had assumed pride of place on social science faculties. Economists’ mathematical rigor and scientific sophistication made them in high demand in public policy and the private sector, which in turn enabled them to leverage their own expertise to claim that science itself dictated they receive higher salaries than their other colleagues in the liberal arts. . . The economy’s supply and demand curves – and all the impersonality and inexorability these entailed – simply demonstrated that economists were scientifically more deserving of higher pay. A claim of merits and just deserts took on the appearance of a value-neutral, descriptive fact.”

Soros scooped Blakely on the topic of economists posing as scientists by about 35 years. That’s the difference between practitioners and professors. Although Soros is a seemingly professorial figure within the world of finance, he could not escape – especially during his heyday – the sheer fact that he had to make money in markets, not just think and talk about them. Being in the market grants insights that cannot be gleaned from the professorial viewpoint. Folks ask me “Evan, you read, write, and think about markets all the time, why not just go get a Ph.D. and be a professor?” My response is “because if I did that I’d be wrong more often than not and not even know it.” Someone like Blakely has to wait for practitioner information to trickle down to his realm of thinking before he could articulate it. As an aphorism, by the time a professor speaks intelligently on a subject, the practitioners are already retired.

Now, does every practitioner recognize what’s really going on in their sector of the market? God no. In fact, I would argue that the vast majority of financial professionals – and almost every equities research analyst – just makes shit up or does not think twice about the world they live in. But they get paid and the world spins madly on, so who cares? Those folks have skin in the game in that they can get fired for being wrong. The same rarely happens to the professorial cohort. For example, McKinsey is allowed to be wrong infinitely more often than your average private equity fund.

Lambert was talking his book when he spoke to Kaminska, but that’s what Tooze does every time he opens his mouth - it’s what we all do. The strange thing here is that the two talkers are of such different worlds that the mere airing of one’s opinion caused a sense of frustration and disappointment in the other. The professorial and the practitioner can’t even talk on the matter.

As I wrote months ago:

“We are all going to die eventually. The question is whether or not the lights will be on when we do.”

It would seem that the wealthy Lambert is concerned that they won’t be. Meanwhile, the comfortably tenured Tooze finds the prospect ridiculous to even consider. Call me crazy for thinking that The Financial Times is in the right for having given a platform to the guy who – even if he’s set to profit from his position – thinks that energy is a worthy thing to worry about during a civilizational transition that we’re cobbling together on the fly.

Perhaps it is merely best to leave with the words of Noam Chomsky on the topic of why he regularly reads, and trusts, The Financial Times.17

“Those who Adam Smith called ‘the masters of the universe’ have to understand the universe. They have to have a tolerably realistic understanding of the world that they are managing and controlling. That’s true of political elites as well, but the business world particularly. Also, the business press essentially trust their audience. They don’t have to impose propagandistic illusions to keep the rabble under control.”

Photo by Patrick Tamosso at Unsplash

https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/insights/eye-on-the-market/future-shock-amv.pdf

https://www.arcenergyinstitute.com/wp-content/uploads/210927-Energy-Charts.pdf, p.8

https://www.bankofcanada.ca/2012/09/dutch-disease/

https://ipolitics.ca/2021/06/18/global-values-must-change-to-rein-in-climate-change-carney/#:~:text=Carney%20hopes%20that%20the%20global,to%20improving%20economies%2C%20as%20well.

Jason Blakely, We Built Reality: How Social Science Infiltrated Culture, Politics, and Power, (New York: Oxford University Press, 2020), xiv.

Ibid, 18.

Donald MacKenzie, An Engine, Not a Camera: How Financial Models Shape Markets, paperback ed., (Cambridge: The MIT Press, 2008), 147-150.

G.B. Madison, “Hermeneutics and Liberty: Remembrance of Don Lavoie,” 141-163, in Jack High (ed.), Humane Economics: Essays in Honor of Don Lavoie, Mercatus ed., (Arlington: Mercatus Center at George Mason University, 2017 [2006]), 144.

Quoted in Ibid, 145.

George Soros, The Alchemy of Finance, reprint ed., (Hoboken: Wiley, 2003 [1987]), 50.

Ibid, 52.

Ibid, 53.

Ibid, 58.

Ibid, 320.

Ibid, 321.

We Built Reality, 10.

https://www.ft.com/content/bcdefd38-3beb-3506-b24c-82285ac87f6c